Participating Whole Life Insurance in Canada: What Happens to Your Dividends?

You have heard that some life insurance policies pay dividends. It sounds almost too good to be true; a life insurance policy that grows while it protects your family. But what does that actually mean, and where does the money come from?

Understanding how dividends work inside a participating whole life policy can completely change how you think about where to put your money.

This Is Not the Same as a Stock Dividend

When most people hear "dividend," they think of a company paying shareholders from its profits. Life insurance dividends work differently, and mixing up the two leads to a lot of confusion.

A dividend on a participating whole life policy is a return of excess premium. Here is what that means in plain terms:

The insurance company charges you more than it actually needs to cover the cost of insuring your life. It collects that excess, invests it inside a participating account — primarily bonds, commercial mortgages, and a blend of equities — and at the end of the year, returns a portion of the surplus back to policyholders. You are not being paid from profits. You are getting back a portion of what you overpaid, adjusted for investment performance.

Dividends are not guaranteed. But Canada's major participating life insurance carriers — including Sun Life, Canada Life, and Manulife — have paid dividends to policyholders every single year for over 100 years. That track record held through the Great Depression, two World Wars, the 2008 financial crisis, and the pandemic.

What You Can Do With Your Dividends

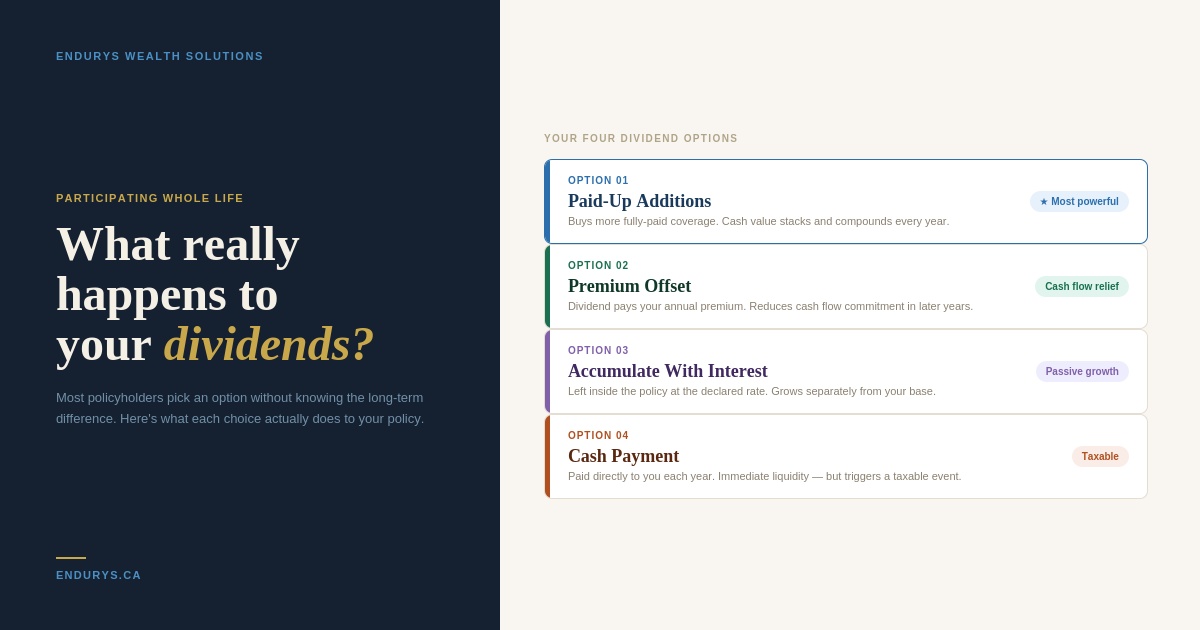

Most participating policies give you several options for how your annual dividend is applied. Each option does something different to your policy, and can have different tax consequences. Understanding the difference is important because this decision compounds over decades.

Paid-Up Additions (PUAs)

This is the most powerful option for most people. Your dividend purchases a small, fully paid-up block of additional life insurance inside your policy. That block immediately has its own cash value and adds to your total death benefit. Because it is fully paid-up, it requires no additional premiums ever. Over time, each year's dividend buys more PUAs, and each set of PUAs has its own growing cash value. The compounding effect stacks year after year. Think of this as a dividend reinvestment plan for your life insurance.

Premium Offset

Once your policy has enough accumulated dividend history, you can use your annual dividend to pay your premium instead of paying out of pocket. This is useful if you want to reduce or eliminate your cash flow commitment in later years of the policy. It’s a way to “turn off” your annual premiums, but still keep your coverage for life. This can reduce the growth in the policy over time, as dividends are not being reinvested back into the policy.

Accumulate With Interest

You can leave dividends inside the policy to grow at the insurance company's declared interest rate. These sit in a separate account from the base policy and the PUAs. They grow, but they do not add to your permanent death benefit the same way paid-up additions do.

Cash Payment

Some policyholders take dividends as a direct cash payment each year. This gives you immediate liquidity but removes the long-term compounding benefit from your policy. This creates a taxable event.

Why Paid-Up Additions Are the Most Powerful Choice

For most people building long-term wealth, paid-up additions are the right choice. Here is why:

Every PUA immediately has two things: cash value and a higher death benefit. Both begin growing from the day they are added. The base policy grows. The PUAs grow on top of it. And each year's dividends buy more PUAs, which grow on top of those.

This compounding within the policy is one of the core reasons participating whole life works so well as a long-term asset. And it is also the mechanical foundation that makes the Infinite Banking Concept work — because as the cash value grows, so does your accessible capital.

The policy is also designed with a built-in guarantee: the cash value must equal the death benefit at the life insured's age of 100. That means the cash value must grow every single day. It is not optional. It is a contractual requirement. That guarantee does not exist in any market-linked investment.

The Bigger Picture

Most Canadians think of life insurance as a cost. A monthly premium paid for protection you hope you never need. A participating whole life policy is different. It is both protection and a growing asset.

The dividend mechanism is what makes that possible. Your premiums fund the protection. The excess gets invested. The surplus comes back to you. And how you direct that surplus determines how fast the asset side of your policy grows.

Understanding this is the first step toward using your policy strategically rather than just holding it.

Ready to Understand What Your Policy Can Actually Do?

Most policyholders have no idea what their participating whole life policy is doing for them year over year. If you want a clear walkthrough — of how dividends, paid-up additions, and cash value work together in your specific situation — let's talk.

[Book Your Free Call → endurys.ca/book]