How to Build a Money System: A Step-by-Step Guide to Controlling Your Cash Flow and Wealth

How to build a money system

Building a money system starts with a budget. A budget is a diagnostic tool that shows you your start state. Money coming in versus money going out including the direction of flow. Where does all that money flow to. The purpose of a budget is to give you clarity on your current financial state. Budgets can be uncomfortable to make because sometimes the truth is scary. That’s okay. It’s important to understand where you are starting from.

We already talked about how goals become the end state in a previous blog. A goal, plus the surrounding conditions that need to be met to declare victory need to be clearly defined. Let me give you an example. If the goal is financial freedom, we now need to define what that means. It could mean that our passive income covers all of our expenses to include; housing, food, utilities, and hobbies. With each of these expenses, we need to come up with an actual dollar amount. Let’s just say its $5,000. Now we have a number associated with the goal.

Notice that the goal is not just a number invested or set aside. Net worth is a meaningless number. Cash flow is what determines how comfortable you will be because a number on a piece of paper doesn’t pay the bills. Cash in our hands does.

Now we will need to flush out the details of that end state a little more including where that wealth is stored, how accessible it is, who controls it, and how we spend it, but to keep this article simple we will leave it at that.

So, the budget is the start state, the fully defined goals are the end state, now we need the system that connects the two.

Step 1 – where does my money reside

The first question that needs to be answered is where does my money reside? This question is a lot more important than you might think. For 99% of the population their money resides inside a bank account. This is very convenient and is safe, but it benefits the bank, not you. Wealth is created by controlling the flow of money so you can profit from that flow. When you leave your money in a bank, they control the flow of money and they get to profit from it. From your perspective, that money is stagnant. Its sitting still doing nothing for you.

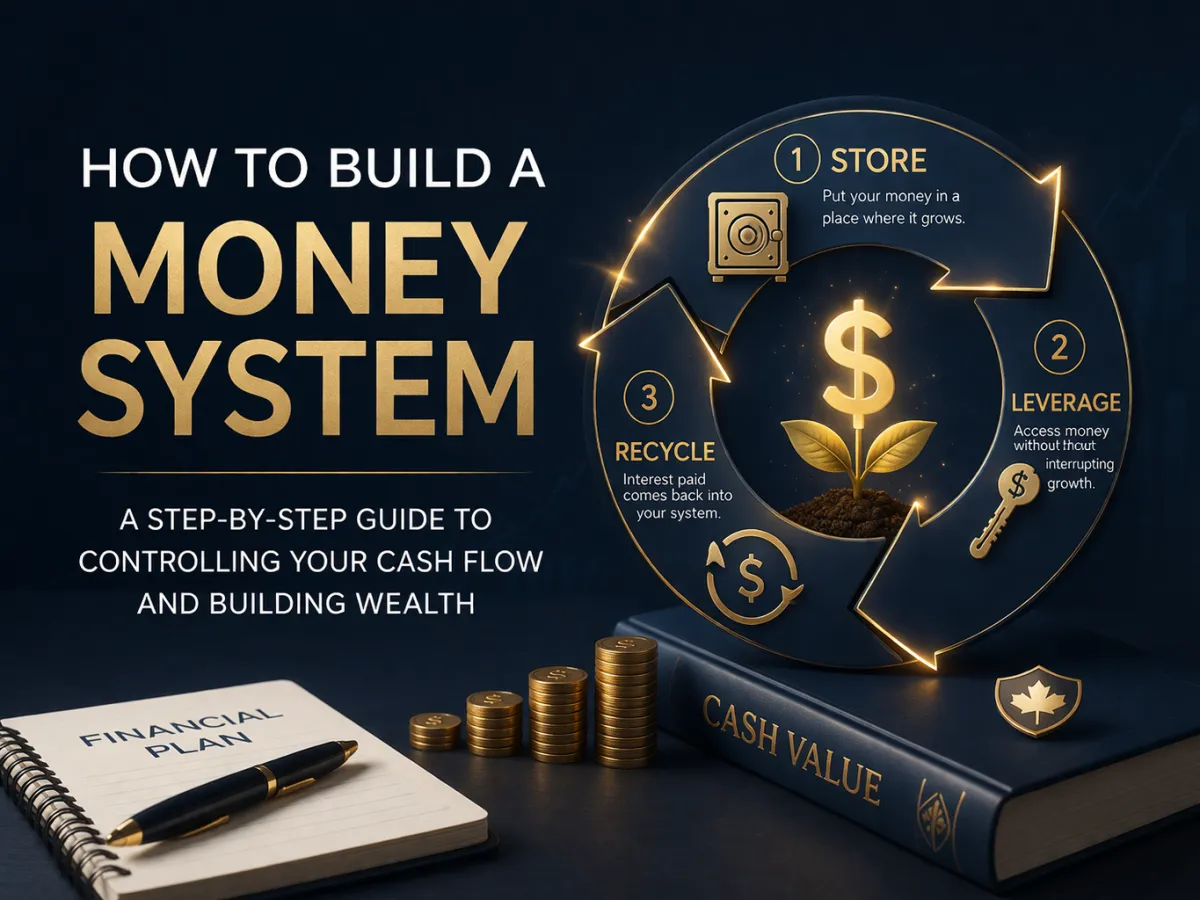

Changing this one thing by itself is going to have a massive impact on your financial life in the long run. Why? Simply because of the fact that your need for financing is going to continue for the rest of your life. You are going to need to buy things in the future. You can either borrow money to pay for these things, and pay interest, or you can pay cash and give up the interest you could have earned with that money. We want to get the best of both worlds. What we want to achieve is a scenario where our money is stored in a place where it can compound and grow uninterrupted while stilling allowing us to leverage against its value so we can access money when we need it. Bonus points if the interest we pay on the borrowed money finds a way back into our pocket.

What this creates is an environment where we can safely store our money, where it can compound and grow, without losing out on the ability to access money when we need it. Instead of storing your money in a bank account where it may grow with interest, but we need to interrupt that growth to access money. We are instead storing our money in a place where it is going to grow, much like it would in a bank account, but instead of interrupting the growth, we just borrow money against the value of the money we have in the account. What this means is we need to use our money to buy assets that will appreciate in value, and are secure enough for us to leverage against.

Yes, you are going to pay interest on the borrowed money, but what if we could create a scenario where we owned the entire lending institution so the interest we pay finds its way back to us? Then we would benefit from the interest being paid to us on account balances and from the interest that we pay on loans.

The goal is to create an enclosed environment where we benefit from every aspect of the flow of money. That way there are no leaks. We put money into the system, and it continues to compound and grow forever. There is no need to interrupt the growth to access money. This can only be achieved by using the right tools. The best tool for the job is a participating whole life policy because it can create this environment.

Instead of a bank account, where the bank gets to use your balance as loans to other people, which then generates interest and ultimately profits for the bank. We can create an environment where our money is inputted into the system as premium. It then compounds and grows uninterrupted in the form of cash value. It grows because contractually the cash value must equal the death benefit at age 100. Then we can leverage against the value of our policy. This means we can borrow up to 90% of the available cash value at any time. Then, when we pay interest on the loan, the life carrier is generating profits. As a participating policy holder, we get to share, or participate, in those profits in the form of an annual dividend. We benefit from every action that takes place in the environment.

This is what it means to put your money in a place where it works for you instead of someone else.

Step 2 – how do we access money

Leverage is when we borrow money using the value of an asset we own as collateral. There are many examples of people using this in everyday life. The most common example is accessing money by offering up the equity in your home as collateral, referred to a home equity line of credit. You get to borrow money without having to sell your asset.

However, should you not repay the loan, the bank now can recoup the cost of the loan by selling the asset that has a lean upon it, in this case your house.

So, while you could buy real estate and store your money in these properties, there is always the potential that your properties could lose value, and you would be forced to sell properties to cover the loans you have.

What we teach people to use is a specially designed participating whole life policy. Why? A properly designed whole life policy is an exceptional place to store money and achieve the balance of growth versus leverage. The cash value, or equity in the policy, cannot go down. Unlike the value of a home which can fluctuate, the cash value can never go backwards because the cash value must equal the death benefit at the life insured’s age of 100.

This is a much more secure asset to leverage against because the value can never go down. This means as we continue to store our money in this asset, we can leverage higher and higher amounts without the fear of having that loan called in. Now you should always repay the loans because interest can compound both for and against us, but this is the most secure asset you could possibly have.

What this does for your financial life is this. We can store our money in a place where it is guaranteed to compound and grow, because the cash value must equal the death benefit. Then we can access money to pay for the things we need in life, like cars, schooling ect. Then as we repay those loans, we have instant access to the principle again. However, our asset has continued to compound and grow in the background meaning the value of our asset is always growing. If designed properly with the right product, this rate of growth on the asset will almost always be faster than interest can accrue on the loan.

Step 3 – continuous use of the system

What does it actually look like to use this system? We’ve already established that paying premium is what creates the equity that we can leverage. Now its not a perfect 1:1 ratio. In fact, for the first few years you will actually lose money before the system starts to become more efficient. The break even point is around the 5 year mark, assuming you are maxing out your annual premiums. However, each year the policy gets more and more efficient. At the 10 year mark, you may get a 1:1.5 ratio. Each dollar of premium you pay gives you access to one dollar and 50 cents. At the 20 year mark it may be 1:2. Each dollar of premium gives you access to two dollars. And it continues to get even better from there.

The reason for this is because this tool is a legitimate life insurance product. The insurance carrier recoups the majority of its costs to implement the policy (advisor commission, admin fees ect) in the beginning years when the risk of payout is the lowest. While not shown on an invoice like most costs, what you see instead is a slower build up of cash value during the beginning years.

As we build up cash value, we can take a policy loan at any time for up to 90% of the available cash value. Each time we take a policy loan, the available cash value goes down. Think of it like a line of credit. If you have $50,000 of credit, and you take a loan for $20,000, you only have $30,000 available to you. Each time we repay a loan, the available cash value is restored, just like it would be with a line of credit. Now its important to note that the cash value continues to compound and grow every single day in the background regardless of if you have a policy loan out or not. This is why we use the term available cash value. You are not withdrawing funds, therefore, we are not interrupting the growth. What this means is every single day, the upper limit of your cash value is increasing. First its $50,000, the next day its $50,005, then $50,010 and so on.

How you use those policy loans is totally up to you. It is great practice to use the loans to finance the things you need in life that you were going to finance anyways. This could include cars, university, renovations ect. Instead of the interest being paid going towards the pockets of the bank or lending institution, they are going back into your system in the form of a yearly dividend.

Better yet, these loans remain completely private. They will not show up on any credit report and will not affect any debt to income ratios required for additional loans should you need them.

This cycle can continue indefinitely. Use it for the remainder of your life to finance whatever you need, and you will recapture all of the interest you were once paying, plus you are generating an annual return on your money every single year.

What does this system give me?

Besides the actual dollar amounts gained from the growth of the cash value and the interest we have recaptured, the true power of using a money system in this fashion is the control it gives you. Because all of the loans are leveraged against a life insurance policy, it is an extremely secure asset. Everyone is going to die one day. Since the contract is set up so that the cash value must equal the death benefit at age 100, and you can not borrow more than 90% of the available cash value, you can never be in a situation where the amount you owe is more than the death benefit of the policy.

A quick side note, you can destroy these policies by borrowing and allowing the loans to compound. This can create a scenario where there is no more cash value available because the compound interest on the loans is exceeding the growth of the policy. In this case, the policy will lapse and you will lose coverage.

Outside of that, what this actually means is that the life carrier knows it is going to get its money back when you die. It also knows that each day you have a loan outstanding, the interest that is generated is a profit to the company. This means that they don’t set any repayment stipulations on the money. What this means to you is that you have complete control over the repayment of that loan.

For example, let’s say you financed a car through a policy loan. You established that the loan for the dealership would have meant a $500 a month payment. So instead of paying the dealership $500 a month, you repay your policy loan at a rate of $500 per month. However, let’s say 6 months after buying the car you lose your job. That $500 a month commitment is now a serious drain on your resources until you can find another job. Well, if you have complete control over the repayment of the loan, can you take a break from the repayments to re-allocate the money towards living expenses until you are back working? Absolutely you can. In fact, assuming the math works out and the compounding interest won’t collapse your policy, you don’t ever have to repay that loan (although we always advice people to pay back loans!)

Control is the true metric that you gain though implementing a system like this. Yes it will make you money, yes its easy and efficient, but the true value lies in not being committed to large financial costs.