How Much Life Insurance Do You Actually Need? A Framework for Canadian

You know you should have life insurance. You might even have some already. But if someone asked you right now whether your coverage was enough, would you actually know the answer?

Most Canadians don't, and that gap can be devastating for the people left behind.

Life insurance is a risk transfer tool. You pay premium to shift the financial risk associated with you passing from your family, to the insurance carrier. You need to understand the full scope of the risk you are transferring before you can get accurate coverage.

The Problem: Most People Are Just Guessing

Here is the uncomfortable truth about how most Canadians end up with a coverage number:

Their employer gave them 1 or 2 times their salary and they accepted it without question

They picked a round number that felt affordable

An agent recommended something and they said yes without knowing how the number was calculated

Two times your salary sounds reasonable until you do the math. For most families, that covers one or two years of living expenses, without covering the cost for a funeral as well. Your mortgage still has 20 years left. Your kids are 8 and 10. That gap is enormous.

There is no shame in not knowing. Nobody teaches this, but there is a simple framework that gets you to a real number in about 10 minutes.

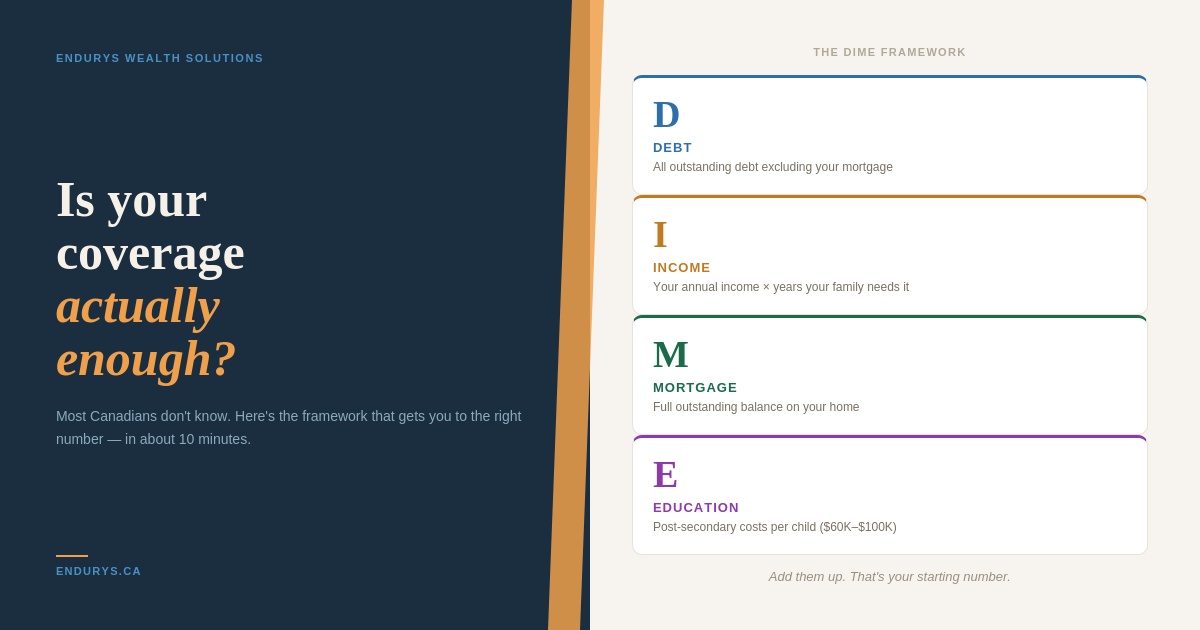

A Simple Framework: DIME

DIME stands for Debt, Income, Mortgage, Education. Add these four numbers together and you have a solid starting point for how much coverage you actually need.

D — Debt Add up everything you owe that is not your mortgage. Credit cards, car loans, personal loans, lines of credit. If you died today, this is what your family would be left holding.

I — Income How many years does your family need your income to stay stable? A commonly used starting point is 10 years. Multiply your annual income by that number.

M — Mortgage Add the full outstanding balance on your home. For most Canadians, this is the biggest number on the list.

E — Education If you have children, estimate what post-secondary education will cost for each one. A conservative estimate in Canada today is $60,000 to $100,000 per child, depending on the school and program.

Add those four numbers together. That is your coverage baseline.

A Few More Things to Consider

The DIME total is a starting point, not a final answer. A few other factors can move the number up or down:

Savings and investments: If you have a solid RRSP, TFSA, or other assets, that reduces how much your policy needs to cover. Your insurance fills the gap between what you have and what your family needs.

Your partner's income: If your spouse earns a strong income and could manage without yours, your coverage needs are lower. If they would be financially vulnerable without you, they need to be covered too.

Your stage of life: A 35-year-old with a large mortgage and young children needs far more coverage than a 58-year-old whose mortgage is nearly paid and whose kids are adults. Coverage needs drop as your obligations shrink.

Your needs will also change over time. A policy you designed at 30 should be reviewed when you buy a home, have children, or change jobs. Life insurance is not a buy it and forget it decision. When done correctly, and strategically, it will have been designed to allow your coverage to grow or shrink as you progress through different life stages.

The Type of Policy Matters Too

Once you know the number, the next question is what kind of policy delivers it most effectively. That comes down to your timeline and your goals.

Term insurance covers you for a fixed period — usually 10, 20, or 30 years — at a lower premium. It works well for covering obligations you expect to pay off over time, like a mortgage or raising children. It is cheaper because the risk of you passing away during the term is low.

Permanent insurance, including participating whole life, covers you for life and builds cash value as it grows. It costs more in premiums but does more than just provide a death benefit because it becomes a financial asset on its own terms.

Which one is right for you depends on your situation. There is no universal answer, and anyone who tells you otherwise is oversimplifying. Most often, we design policies to have both term and permanent coverage.

Ready to Figure Out Your Number?

If you have never run these numbers before — or if you are not sure whether what you have is still enough — I can walk you through it.

Book a free 30-minute call with me at Endurys Wealth Solutions. We will look at your situation together, run through the numbers, and I will show you what coverage actually makes sense and what type of policy fits your life.

[Book Your Free Call → endurys.ca/book]

Sources

Financial Consumer Agency of Canada — Life Insurance — Government overview of life insurance types, how they work, and key considerations for Canadians

Canadian Life and Health Insurance Association — Industry body representing Canadian life and health insurers; publishes annual facts and figures on coverage trends in Canada

FCAC — Buying Life Insurance — Practical guidance from Canada's federal financial consumer agency on how to evaluate and purchase coverage