The Bucket Analogy: How Control, Not Income, Determines Your Financial Future

The Bucket Analogy

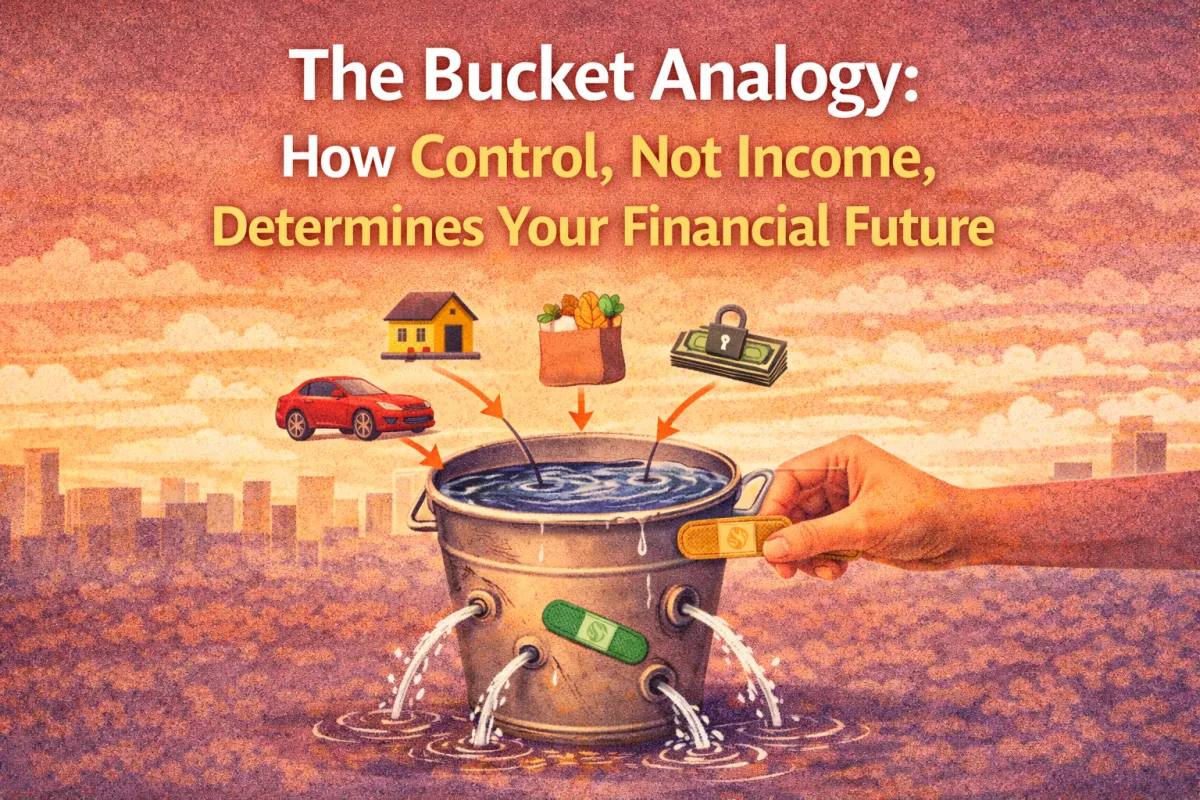

Suppose you have a bucket. This bucket represents your lifetime financial goals. When the water in the bucket reaches the top, congratulations you have achieved all of your financial goals! The catch is, each time you allocate money to a source other than achieving your lifetime financial goals, you create a whole in the bottom of your bucket. Some holes are big, such as a mortgage, and some are small, such as hobbies, but the holes add up.

Each month all of us receive some form of income. We then divide that income up into the piles we need to pay for the things we have in our lives. Groceries, bills, entertainment, cars, house, investments etc. Each of these line items represent a hole in your bucket.

The point isn’t to see all of these expenses as just a drain on your system, it’s more about understanding that each of these expenses represents a loss of control of your money, which results in it being drained away. Each time you pay one of these expenses, you give that money away and never see it again. It is gone. It is no longer working towards filling your bucket and achieving your financial goals.

Most people, as they go through life and make more money, add more holes to their buckets. More water may be coming in to the bucket, but we have added more holes as well. What implementing a personal banking system does, is start patching those holes.

When you start patching those holes, your bucket starts to fill that much faster. How do we patch a hole? We simply take back control over that portion of money, or in this example water, that was leaving us.

We then use someone else’s flow of water to pay that expense. In the context of Infinite Banking, we use the life carrier’s money in the form of a policy loan. This allows us to patch that hole, meaning the water that was leaving our system is now working towards filling our bucket.

How do we repay the water we are borrowing? Well, we can dip a cup into our bucket to repay them, but we control the cup. We control how much water we put into the cup, we control when we fill the cup up, therefore we control the repayment schedule. With a hole in the bucket there is nothing you can do to change the outcome of water flowing through it.

By patching the hole, it also means that we are taking water out of the collective bucket rather than letting it drain out of a hole. What I mean is if we think of a budget as a tool to divide our resources up to pay for the things we need in life, then we are deliberately separating those actions. We can’t use retirement savings to pay for groceries or the car payment to pay for investments. If it was all in one communal bucket however, it no longer matters what the original purpose of the water was. Only that there is water in the bucket. Let us look at a few line items in our budget and determine what they are for as an example.

Let’s look at retirement savings. The purpose of this line item is to put money in a place where it will compound and grow uninterrupted with the goal of it growing enough that it can sustain the lifestyle we want later in life when we stop receiving a conventional income. The main question I have is, how does that money help you right now? How does it help with buying a car? Or financing a family vacation? The true answer is, it doesn’t. We sacrifice those things now, so we can sustain ourselves later. We do this because we have to. Without owning the entire banking system, you cannot bridge the gap between being the depositor and the borrower so we are forced to make holes in our bucket to survive.

What happens if we do own the entire system though? We know that the deposits we put into our system are left untouched so they can compound and grow uninterrupted. We never labeled what the deposits were for because their only goal was to capitalize the system, or build up enough equity so we can borrow against it on the other side. With this logic, we can see that our retirement savings can absolutely be used to fund a car, or a vacation or a hobby! We have simplified our finances by plugging all the holes in our bucket. All of our income goes towards building wealth within our system. Then we borrow against those deposits and use someone else’s money to pay for the things we need in life.

A quick side note. I have referenced using retirement savings to capitalize your system. In order to reconcile this thinking, we need to understand the purpose of savings. The goal of retirement savings is to create a vast pile of wealth that can sustain our lifestyles once we are no longer actively generating income from working.

Putting your money in a place where it is going to compound and grow, uninterrupted for decades, is going to achieve the same results. However, what we haven’t discussed yet is the flexibility awarded to the bank owner on how they access this money in retirement. We will get into this later in the book, but what you should covet is growth and flexibility in your retirement plan rather than just growth. The tool we use to create a banking system gives you that.

Of course, we have to be a responsible banker and we must have a plan to repay that money, because interest can compound both ways. What this creates though, is two inputs into our system. We have deposits, which grow our system, and we have repayments that replenish our system. That’s it. The water inside of that bucket represents the liquid capital we have access to. There are no holes in our bucket, but when we borrow from our system, it represents us taking a cup, dipping it into the bucket, and removing some of the capital we have access too. As we repay that loan, we put the water back into the bucket. What we have created is a system where we have two different and distinct streams of water being used to fill our bucket, with no leaks, and only one way to remove the water.

But here’s the thing, we have absolute control over the cup that borrows our water. We control when the cup comes to take the water, we control how much water it takes. Unlike a hole in our bucket where we have no control. A hole in the bucket will continually drain our water whether we want it to our not.

With this logic, we have created an and in our financial vocabulary. We can save for retirement and a family trip. We can save for a new car and fund a new hobby. We have added utility to our money, meaning we can use it for more than one thing, while simultaneously simplifying our finances. What we end up with is a very sturdy bucket that fills much quicker than before, and suddenly has much more water available to us when we decide we need it later in life.

This isn’t to say that you need to stop investing in your future through whatever means you are currently doing. Whether its in real estate, stocks or something else. It just means that if you run it through your system first, your money can be put to work building your future and financing the needs you have now.